Updated July 6, 2023

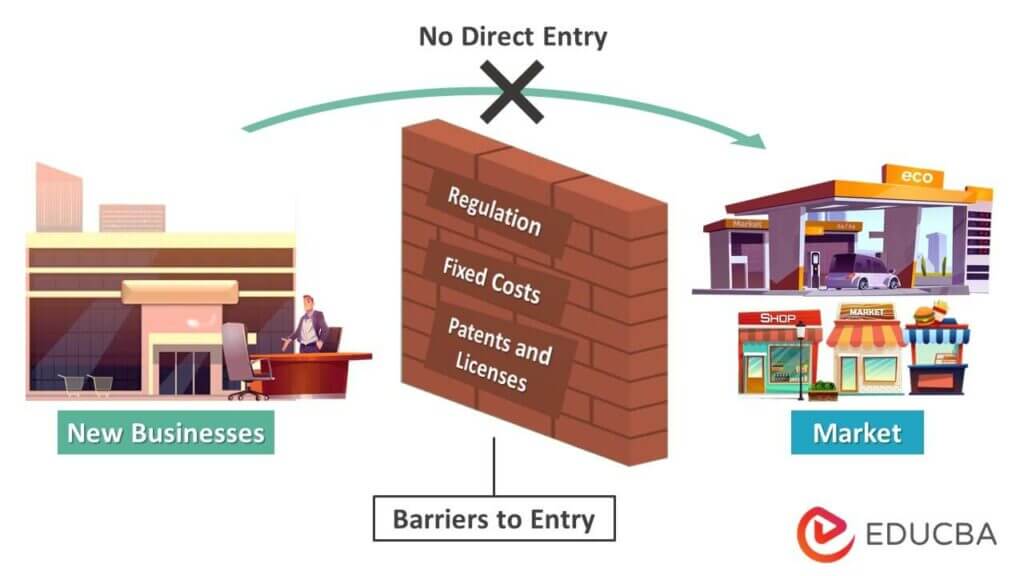

What are Barriers to Entry?

Barriers to Entry are the obstacles a company may face while starting a business in a new industry. These barriers can be startup & fixed costs, patents, technological issues, etc.

For example, if an industry has one or two well-known brands with a loyal customer base, it can become challenging for new companies to compete. This represents the brand recognition barrier.

Companies must be aware of the barriers while entering a new market. Before venturing into a new product, new companies can speculate on aspects like regulatory, legal, technical, Strategic, and brand loyalty. There could also be hindrances, such as licensing or education requirements, workforce, infrastructure, etc.

Key Highlights

- Barriers to entry are economic interruptions that a new business faces while entering a specific market.

- The barriers can be financial, technological, natural resources-based, political, or legal.

- Different markets may have different competitive dynamics, so companies should assess their competitive landscape carefully before entering, including high capital requirements or the need for specialized knowledge.

- Companies should devise a clear plan to overcome these potential barriers to be successful.

Examples of Barriers to Entry

Example #1: Smartphone Market

Samsung, with its large screen, and Apple, with a face ID, have dominated the smartphone market for the past decade. However, with new technologies like foldable displays and 5G networks, we are seeing a shift in power in this industry.

However, these technologies are acting as barriers for new technology startups. The new companies will have to launch something similar or advanced to what the market already has.

Example #2: Retail Banking Sector

The retail banking sector is one of the most competitive in the financial industry, with a pervasive network, making it impossible for a new entrant to compete with the already established players.

Types of Barriers to Entry

Patent

- When the government backs up barriers to entry, it is called a patent.

- The company gets the special rights to produce a particular good for a specified period. It prevents competitors from entering the market.

- Pharmaceutical and technology fields often get patented goods.

Economies of Scale

- As a business grows, it enjoys reduced cost prices. For example, Grocery stores can get basics like milk and bread at lesser prices, whereas smaller shops do not have that privilege.

- The new businesses are disadvantaged as bigger supermarkets can negotiate for lower prices because of their big orders and size, and competing is hard for small ones.

Sunk Cost

- It is the necessary cost an entrant must make and is unrecoverable.

- They must invest in office space, electricity, advertising and marketing, R&D, technology, etc.

- Since it is impossible to recover these costs, a company may be discouraged from making the first investment.

Technological Advancement

- Starting a new business, owners need to have a specific know-how level. One can work in supermarkets and learn the nitty-gritty before owning one.

- Companies like software and airlines have a bit of a knowledge barrier.

- The software business owner should either be an expert or hire a coder.

Brand Loyalty

- For instance, brands like Coca-Cola or Nutella are essentially unmatched in their quality and price, making it impossible to compete with a company that has historically invested worth trillions in establishing itself.

- Consumers have formed a habit of trusting these brands.

Difficulties in Changing Suppliers

- In some markets, consumers feel restrained because of the procedures required to switch suppliers.

- For example, the banking, insurance, and electricity industries are too complicated.

Control Over Distribution Channels

- Some businesses, like Amazon, have complete control over their channels and distribution networks, making it difficult to find their rivals.

- Due to its endless choice and display of products in each category that fits all pockets, customers have to look no further.

Business Response Tactics

- The existing established players try to block the new companies from entering the market.

- A based business may lower prices or run aggressive promotions in response to a competitor’s entry attempt.

Regulation

- Regulations require extra cost, time, and effort before a business can catch momentum. A restaurant owner must handle many health and safety regulations besides others.

- Often companies have to hire a lawyer. When a new entrant enters the market, the existing ones may create additional barriers for them by offering benefits or offers to the targeted customers.

Importance of Barriers to Entry

Increased Profitability

- Existing businesses can enjoy increased profitability by making it harder for new competitors to enter the market.

- Their cost of production stays low, and demand for their services remains high.

Brand Recognition

- With fewer competitors in the market, existing businesses can benefit from increased brand recognition and credibility.

- Customers will be more likely to seek out their services due to their reputation.

Established Footprint

- Established businesses can protect their place in the market by using barriers to entry.

- They prevent new competitors from undercutting them on price or offering better products or services.

- It helps preserve its customer base and market position.

Security of Investments

- Existing businesses can protect their investments and assets from devaluing by creating barriers.

- They prevent new competitors from entering the market with deeper pockets and more resources from taking their investments.

Reduced Price Wars

- With fewer competitors in the market, price wars are less likely to occur as businesses become more difficult to undercut each other’s prices.

Advantages & Disadvantages of Barriers to Entry

|

Advantages |

Disadvantages |

| It allows you to maintain your competitive advantage in the market, making it difficult for competitors to enter. | Barriers to Entry can make it difficult for new businesses to compete against established ones. |

| It enables businesses to control the supply of goods and services to maximize profits. | It can be challenging for those who do not have the capital required to start a business. |

Final Thoughts

Barriers to entry are essential in the business world. With the barrier, there is no competition for your product or service. Thus, monopolies do not worry about anyone undercutting them. It is crucial to remember that the barriers for startups are much lower than they used to be, thanks to new technologies like machine learning.

Frequently Asked Questions (FAQs)

Q1. What are the barriers to entry?

Answer: Barriers to entry is a phrase used to describe the difficulty of starting a business in a specific market. It refers to the minimum amount of capital or other resources needed for someone to create a new business venture. This term applies to startups and entrepreneurship. It can also refer to any barrier preventing someone from starting a new venture, such as a lack of relevant experience or knowledge, lack of access to funding, or lack of connections.

Q2. How to avoid market entry barriers?

Answer: One can use two strategies to get past the barriers to entry: innovation and new distribution channels. The likelihood of entering a closed market increases with the innovation’s disruption. Examples include Tesla automobiles or Dyson vacuum cleaners. Additionally, Selling pairs of glasses or shoes online was unheard of a few years ago. However, outsiders have succeeded in establishing themselves.

Q3. What are the main barriers to entry?

Answer: The main barriers are Economic obstacles, scale and scope economies, product differentiation, substantial capital requirements, legal impediments, and concentration of strategic assets.

Q4. What are the examples of barriers?

Answer: Here are some entry-level obstacles: Governmental rules, contractual requirements, high prices, patents, overpopulation of suppliers, State involvement, and insufficient experience.

Q5. What are the characteristics of tariff barriers?

Answer: Barriers are instruments of control that also produce international rules, allowing you to determine whether a product is regulated and legal. But in many nations, it works against them, and they struggle with new economic development. The least developed countries, including Chad and the Bahamas, have the highest tariff barriers.

Recommended Articles

It is a guide to Barriers to Entry. To learn more, please read the following articles