Updated July 21, 2023

Definition of Cycle Counting

Cycle counting is a periodic analysis of inventory in a storage location which is conducted through the counting of samples instead of physically counting the entire inventory available so as to quickly have an accurate estimate of the inventory available without causing a stop to the day-to-day working as is the case with physically counting every unit.

Inventory Record Methods

There are broadly two methods of keeping track of inventory, perpetual inventory system, and periodic inventory system. Under a perpetual inventory system, every inflow and outflow is recorded in real-time as it happens, and therefore proper bookkeeping is maintained for this process.

Whereas, in the case of periodic inventory management, according to the need of the company, at periodic intervals, the inventory is calculated and tallied with sales and purchase records to get the stock of the goods. This process is a tedious and time-consuming one, and therefore many organizations implement the Cycle counting procedures, where they implement the sampling method instead of counting each unit.

Types of Cycle Counting

There are several types of cycle counting processes, as described below:

1. Control Group

This method is applied in the initial phases of cycle counting because this is the time when a proper counting methodology is being formulated for the specific organization under analysis. Here the same groups of items are counted several times during a short period of time to understand the in and out movements of these items and then come up with an optimum counting technique and eliminate the counting errors that are being committed over time.

2. Random Sample

This practice is useful when the storage has several items of one kind stored here. If, at a time, there are several units of one kind available, then the organization gets a fair idea of how much stock it has and, therefore, can pre-empt shortage and order requirements based on the periodic cycle counts.

3. ABC Analysis

Under this company, specific categories are formulated, and items are put under these categories. Generally, 3 categories are formulated; category A items are counted more frequently and generally comprise fast-moving items. Category B items are counted less frequently, and category C items are counted even less frequently. There can be more categories as per the need, size, and variety of the inventory; however, this format of counting is generically termed ABC analysis.

Cycle Counting Procedure

Having understood the concept of cycle counting, the natural question that follows is that if we are sampling inventory, then what should be the basis of doing so, and how frequently should we conduct the counting exercise to have a true and fair idea of the stock without compromising the day to day working, which is the basic premise of why cycle counting is being conducted. For these reasons, there are various techniques have been formulated over time:

1. Pareto Method

In this method, those items which cost more and are used up more frequently are counted more often than others. For this purpose, the consumption is valued by multiplying the items used in a given period of time with the cost of each item, if so available, or an average cost of the items that can be derived from past purchase records. Those items which have higher value are counted more frequently, and therefore this method essentially bifurcates the inventory into two categories high value and low-value items.

2. Frequency Based Counting

In this method, those items which are used up more frequently are counted more often without paying attention to the value of these items. It is a more prudent approach that doesn’t distinguish between high-value and low-value items and works on the philosophy that each time inventory is purchased or sold, there could be a possibility of error in recording, and therefore, those which have a greater possibility of such error, are overseen with greater frequency.

3. Combination or Hybrid Counting

This is a combination of the Pareto technique and the ABC counting method, where the first level of bifurcation is made based on the value of the items while the second level of categorization is made based on ABC counting wherein, further sub-categorization is made based on several criteria such as high demand item or seasonal items or low shelf life items or even based on customer urgency requirement and so on. Such categorization can’t be completely automated and requires human intervention because several items might fall into more than one category and therefore require a specific counting frequency.

4. Surface Area Based Counting

At times it is also known as objective counting because here, we only look at the empty spaces which need to be filled, and in doing so, we aim at quickly filling these empty spaces. Such a method might be more suitable in a supermarket that is properly mapped out and methodically arranged.

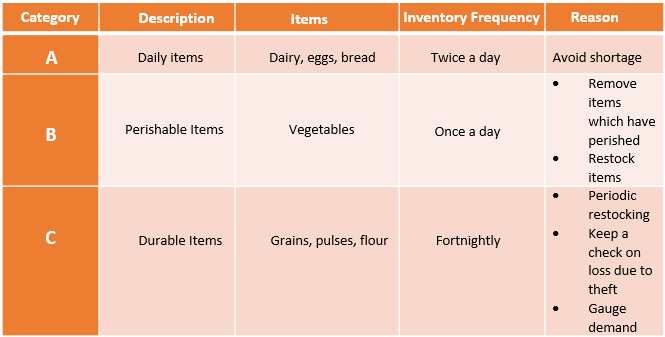

Example of Cycle Counting

Let’s take the example of a supermarket. There are various kinds of items which are divided into the following categories:

- Daily items: Dairy, eggs, bread, etc.

- Perishable items: Vegetables

- Durable items: Grains, pulses, flour, etc.

The supermarket wants to have an inventory management system in place so that it reorders quantities optimally. So the store manager has come up with the following categories and inventory management techniques:

This is quicker as compared to the physical counting of all items each day.

Difference Between Cycle Counting and Physical Inventory in Oracle Apps

- Scheduling: Scheduling cycle counting is possible while scheduling physical inventory is not possible

- Disruption: During counting, the stack is visible in the system if the cycle counting is implemented, but it is not the case when implementing physical counting

- Transaction Freezing: Inventory undercounting can be transacted upon in cycle counting, while this is not the case with physical counting

- Record: Previous counting records are available in the cycle counting method but not in the physical inventory method

Benefits

- Quick: In organizations that can’t manage perpetual inventory, the periodic system is followed; however, it is highly time-consuming. Therefore, Cycle counting speeds up the process.

- Cost-Effective: As a perpetual inventory system requires proper accounting and bookkeeping, therefore, the method is very costly as it requires a skilled workforce and also expensive software. On the other hand, the cycle counting approach can be achieved through a lesser costly workforce by providing proper training.

- Doesn’t Cause Disruption: In the case of periodic inventory management, the daily working is stopped during the period when counting takes place. This doesn’t happen in the case of cycle counting as the process is broken into parts and conducted department wise and not for all the inventory together.

Disadvantages

- Less Accurate: As this method relies on sampling, it is not completely accurate, and before achieving the desired level of accuracy, several iterations of counting are required, which might not give the required result on completion.

- Procedure to Be Followed: Initially, when the cycle counting is implemented, the beta and pilot testing needs to be thorough and rigorous so that a proper sampling technique is defined because if this is flawed, cycle counting will not give proper results.

Conclusion

Overall, Cycle counting is an attempt to reduce the effort of physical counting under the periodic inventory method without disrupting the day-to-day operations using the appropriate sampling technique as per the requirement of the organization under consideration. It is helpful in the case of those organizations which don’t have the resources to maintain a perpetual inventory system. However, there are chances of a lack of accuracy in this method if the sampling technique is erroneous.

Recommended Articles

This is a guide to Cycle Counting. Here we also discuss the introduction and several types of cycle counting processes along with benefits and disadvantages. You may also have a look at the following articles to learn more –