Updated February 15, 2023

Difference Between Direct vs Indirect Cash Flow Methods

The cash flow statement is the financial statement that describes the cash flow movement happening in the business from one financial period to another financial period. The cash flow statement can be prepared by utilizing two broad methods namely the direct cash flow method and the indirect cash flow method. The main difference between the direct and indirect cash flow statement is that in direct method, the operating activities generally report cash payments and cash receipts happening across the business whereas, for the indirect method of cash flow statement, asset changes and liabilities changes are adjusted to the net income to derive cash flow from the operating activities.

The cash flow statement is generally regarded as the third most critical financial statement after the balance sheet and the income statement. The balance sheet shows the financial position of the business for a given financial period. The income statement reports the revenues and expenses for the given financial period. Lastly, the cash flow statement describes the movement of the cash happening in the business for a given financial period wherein this statement is derived using the components of both the income statement and balance sheet.

The cash flow statement is a critical statement as it helps the stakeholder evaluate the cash flow position of the business. Generally, a cash flow statement is composed of cash flow from operating activities, financing activities, and investing activities. For the direct and indirect methods of cash flow, the cash flows arising from the financing activities and investing activities tend to be the same. However, the approach utilized for the cash flow from the operating activities differs for both the direct method of cash flow statement and the indirect method of the cash flow statement. As per the directives of the US reporting rules, the business or an organization or a corporation for to say rests with the option to choose either indirect method of the cashflow statement or direct method of cashflow statement. Furthermore, the indirect method of the cashflow statement takes a lot of time in preparation and also displays some level of accuracy issues as such statement utilizes a lot of adjustments. The direct method of the cashflow statement, on the other hand, remains to be most potent way of preparing cashflow statement and it takes less time to prepare the statement as the adjustment, as well as segregation of the cash-based transactions over the transactions that are non-cash, are absent. Basis this attribute, it generally presents a more accurate picture of cashflow position of the business as compared to the indirect method of the cashflow statement. Despite having the attribute of accuracy in the direct cashflow statement, it is utilized less by the business and enjoys less popularity. On the contrary, the indirect method of the cashflow statement is far more popular among the accountants and most used methods to arrive at the cashflow statements.

Head to Head Comparison between Direct vs Indirect Cash Flow Methods (Infographics)

Below are the differences mentioned:

Key Differences between Direct vs Indirect Cash Flow Methods

The key differences between the Direct vs Indirect Cash Flow Methods are as follows:

The indirect method is relatively complex method as compared to the direct method as it utilizes net income as the base and performs necessary cashflow adjustments. One of the adjustments can be regarded as the treatment of non-cash expenses. In indirect method, depreciation which is a non-cash expense is generally added back to the net income followed by additions and deductions arising from the changes in liabilities and assets.

In direct method, on the other hand, no such adjustments are performed. More broadly, the cashflow from operations is prepared by accounting for cash receipts and payments of the cash in case of the direct method. The cash receipt is generally recorded as the receipts from the customers and the cash payments are broadly recorded in terms of payments to the suppliers, employees and payments made to service the taxes, interest expense, and other expenses.

However, the direct method completely ignores the application of non-cash transactions such as the treatment of the depreciation expense and the impact on the resulting cash flow. Basis the requirement of compliance and reporting, the business has to choose either one of the methods to arrive at the cash flow from operations.

Direct vs Indirect Cash Flow Methods Comparison Table

Below are the differences :

|

Direct Cashflow Method |

Indirect Cashflow Method |

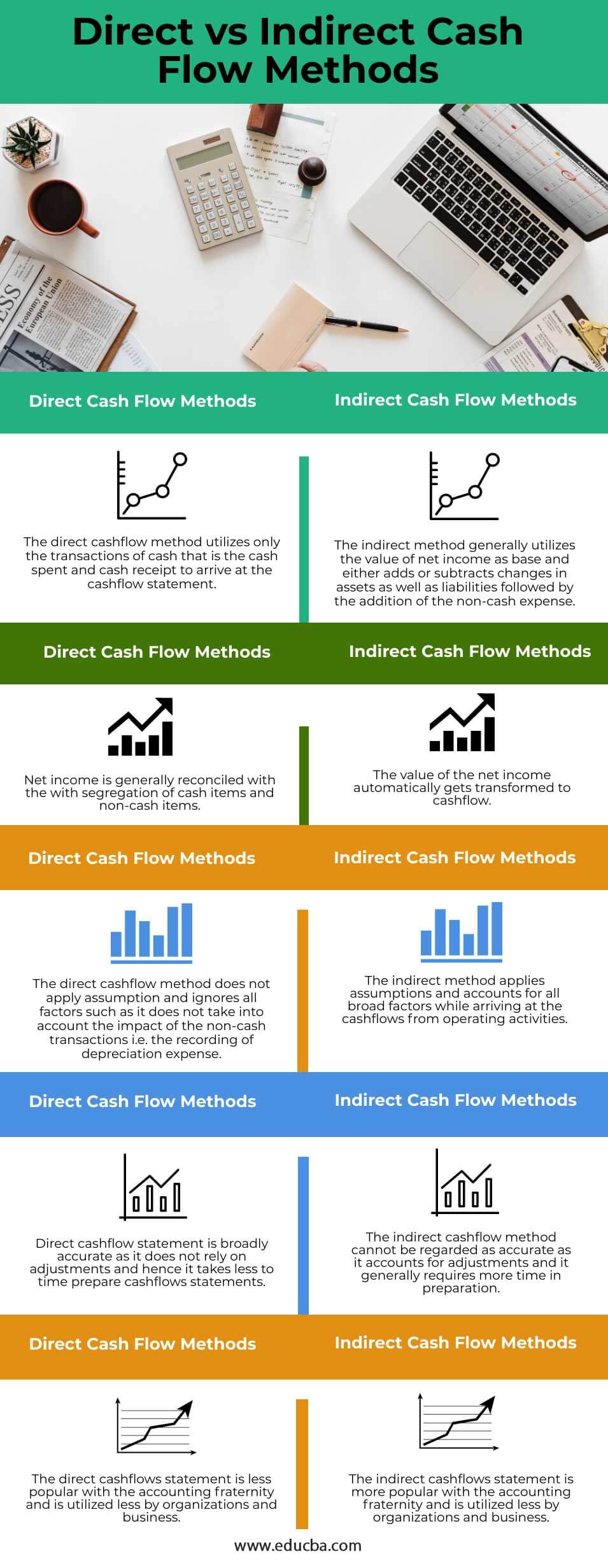

| The direct cashflow method utilizes only the transactions of cash that is the cash spent and cash receipt to arrive at the cashflow statement. | The indirect method generally utilizes the value of net income as base and either adds or subtracts changes in assets as well as liabilities followed by the addition of the non-cash expense. |

| Net income is generally reconciled with the with segregation of cash items and non-cash items. | The value of the net income automatically gets transformed to cashflow. |

| The direct cashflow method does not apply assumption and ignores all factors such as it does not take into account the impact of the non-cash transactions i.e. the recording of depreciation expense. | The indirect method applies assumptions and accounts for all broad factors while arriving at the cashflows from operating activities. |

| Direct cashflow statement is broadly accurate as it does not rely on adjustments and hence it takes less to time prepare cashflows statements. | The indirect cashflow method cannot be regarded as accurate as it accounts for adjustments and it generally requires more time in preparation. |

| The direct cashflows statement is less popular with the accounting fraternity and is utilized less by organizations and business. | The indirect cashflows statement is more popular with the accounting fraternity and is utilized less by organizations and business. |

Conclusion

The direct method of the cashflow and indirect method of cashflow are variants of the cashflow statements. The corporation has the option of selecting either method for the purpose of reporting. It purely depends on the situation at hand and compliance requirements that the business has to meet up in terms of reporting and regulatory standards. The popularity of the indirect method of the cashflow generally exceeds with respect to the direct method of the cashflow.

Recommended Articles

This is a guide to Direct vs Indirect Cash Flow Methods. Here we also discuss the introduction and direct vs indirect cash flow methods key differences. You may also have a look at the following articles to learn more –