Introduction to Getting a Business Loan

A business loan is essential for starting, growing, or maintaining your business. Understanding the process and taking the right steps can increase your chances of securing the funds you need. Consulting a commercial finance broker can offer valuable advice during the process, helping you explore loan options and find the best deal for your business. This guide explains how to get a business loan, covering loan types, preparation tips, the application process, and advice to improve approval chances.

Types of Business Loans

Before applying for a loan, it is important to know the different types available. Each loan serves a unique purpose and has different terms.

#1. Term Loans

In a term loan, a lump sum is borrowed and repaid with interest over a period. There are two main types:

- Short-term Loans: Typically repaid within a year, these loans are ideal for covering immediate expenses or bridging cash flow gaps.

- Long-term Loans: Repaid over several years, these loans are suited for large investments like real estate or equipment.

#2. Equipment Financing

Equipment financing is an ideal option if your business needs to purchase machinery, vehicles, or technology.

- Secured by Equipment: The loan is secured by the purchased equipment, often resulting in better interest rates.

- Leasing Option: This allows businesses to use equipment without purchasing it outright, with the option to buy at the end of the lease.

#3. Working Capital Loans

These loans help cover day-to-day operational costs such as payroll, rent, and utilities.

- Short Repayment Period: They typically have short repayment periods, which are ideal for covering immediate expenses.

- Secured or Unsecured: Depending on your business’s financial health, these loans can be secured (requiring collateral) or unsecured (based on creditworthiness).

How to Prepare for a Business Loan Application?

Being prepared is important to increase your chances of approval. Lenders assess various factors to ensure the loan is a safe investment, so understanding these requirements is essential.

1. Define Your Loan Purpose

Knowing how to use the loan will help you choose the right loan type and communicate more effectively with lenders.

- Determine the Amount Needed: Be clear about the specific amount you need and how it will be used (e.g., expansion, inventory, equipment).

- Create a Budget: A well-prepared budget shows how the loan fits into your financial picture, demonstrating repayment ability.

2. Evaluate Your Business’s Financial Health

Lenders assess your business’s financial strength, focusing on:

- Credit Score: A good business and personal credit score shows lenders that you are a lower risk.

- Revenue and Cash Flow: Lenders will look at your business’s revenue stability and cash flow to ensure you can handle regular loan payments.

3. Gather Documentation

Lenders require specific documents to process your application:

- Financial Statements: Please provide the balance sheets, income statements, and cash flow statements for the past two years.

- Tax Returns: To verify your financial history, provide two to three years of business and personal tax returns.

- Business Plan: A detailed business plan outlining your growth strategy, financial projections, and how the loan will contribute to your success can boost lender confidence.

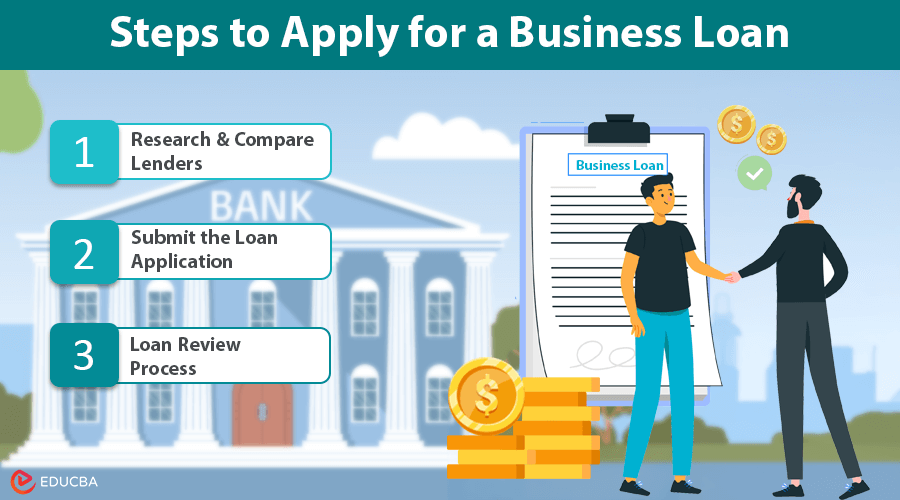

Steps to Apply for a Business Loan

Once you are prepared, the application process becomes much smoother. Here is a step-by-step breakdown of how to get a business loan:

Step 1: Research and Compare Lenders

Lenders have different requirements and offer various terms, so compare your options to find the best fit.

- Banks: Traditional banks offer lower interest rates and longer repayment terms but have stricter requirements.

- Online Lenders: These lenders provide faster approval, but their interest rates are generally higher due to convenience.

- Government Programs: Some government-backed loans offer favorable terms, especially for small businesses or specific industries.

Step 2: Submit the Loan Application

Once you have chosen a lender, apply with all the required documents.

- Online or In-person: You can apply online for speed or in-person for detailed guidance from bank representatives.

- Provide Accurate Information: Ensure your application is consistent with your financial documents, as discrepancies may cause delays or denials.

Step 3: Loan Review Process

After applying, lenders will review your financial information and assess your eligibility.

- Credit Assessment: Lenders evaluate creditworthiness by examining your credit score, financial statements, and overall stability.

- Collateral Evaluation: If the loan is confirmed, lenders will evaluate your collateral to ensure it covers the loan amount if you default.

- Risk Analysis: Lenders will analyze the risks associated with your business and its industry.

Tips to Increase Your Chances of Getting Loan Approval

Here are some tips to increase your chances of getting approved for a loan:

Tip 1: Improve Your Credit Score

A good credit score is important for getting a loan approved.

- Pay Bills on Time: Pay all bills on time to avoid late payments that could harm your credit score.

- Minimize Current Debt: Reducing your debt load improves your debt-to-income ratio and makes you more appealing to lenders.

Tip 2: Build a Strong Business Plan

A detailed, realistic business plan increases your credibility with lenders.

- Include Financial Projections: Provide projected income and expenses, showing how your business will grow and manage finances.

- Outline Loan Usage: Specify how you will use the loan funds, demonstrating responsible planning.

Tip 3: Establish a Good Relationship with Your Lender

A strong relationship with your lender can help smooth the loan application process.

- Open Communication: Be transparent with the lender about any major business changes or financial challenges.

- Request Feedback: If you deny my application, I will ask for feedback to identify areas for improvement in future applications.

Final Thoughts

Learning how to get a business loan involves preparing, understanding the available loan types, and demonstrating financial responsibility. By understanding your needs, choosing the right loan, and getting the required documents ready, you will improve your chances of approval. If your first attempt is unsuccessful, take feedback into account and explore alternative funding options.

Recommended Articles

We hope this guide on “how to get a business loan” has been helpful. Check out these recommended articles for more tips on securing financing and growing your business.