Levered Beta Formula (Table of Contents)

What is Levered Beta Formula?

The term “levered beta” refers to the systematic risk of a company stock that is primarily used in the computation of the expected rate of return using the capital asset pricing model (CAPM).

In other words, levered beta takes into account the impact of the company’s debt level compared to its equity on its systematic risk exposure. Levered beta is also known as equity beta. The formula for the levered beta can be derived by multiplying the unlevered beta (a.k.a. asset beta) with a factor of 1 plus the product of the company’s debt-to-equity ratio and (1 – tax rate). Mathematically, it is represented as,

Examples of Levered Beta Formula (With Excel Template)

Let’s take an example to understand the calculation of Levered Beta in a better manner.

Levered Beta Formula – Example #1

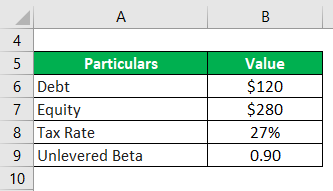

Let us take the example of a company named JKL Inc. to illustrate the computation of levered beta. It is a public listed company and as per available information, its unlevered beta of 0.9, while its total debt and market capitalization stood at $120 million and $380 million respectively as on December 31, 2018. Calculate the company’s levered beta if then the applicable tax rate is 27%.

Solution:

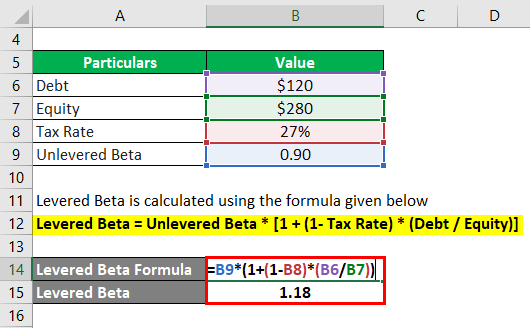

Levered Beta is calculated using the formula given below

Levered Beta = Unlevered Beta * [1 + (1 – Tax Rate) * (Debt / Equity)]

- Levered Beta = 0.9 * [(1 + (1 – 27%) * ($120 million / $380 million)]

- Levered Beta = 1.18

Therefore, the levered beta of JKL Inc. stood at 1.18x as on December 31,2 018.

Levered Beta Formula – Example #2

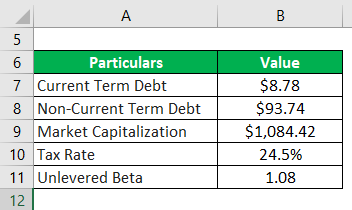

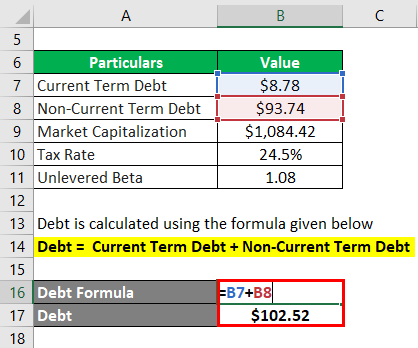

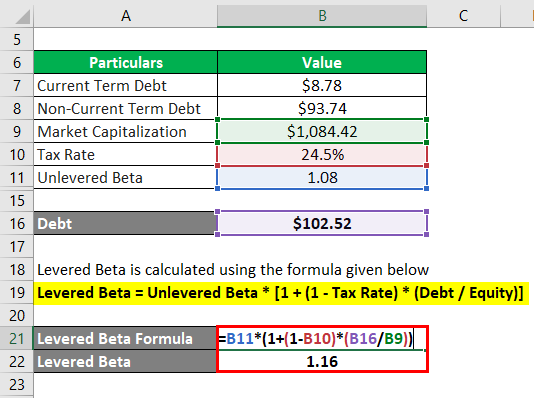

Let us take the example of Apple Inc. to demonstrate how levered beta is computed for real-life companies. According to information available at one of the stock market database, the 1-year unlevered beta of the company’s stock is 1.08. On the other hand, the company reported current term debt and non-current term debt of $8.78 billion and $93.74 billion respectively as on September 29, 2018. The current market capitalization is $1,084.42 billion. Calculate levered beta for Apple Inc. given that its effective tax rate for 2018 was 24.5%.

Solution:

Debt is calculated using the formula given below

Debt = Current Term Debt + Non-Current Term Debt

- Debt = $8.78 billion + $93.74 billion

- Debt = $102.52 billion

Levered Beta is calculated using the formula given below

Levered Beta = Unlevered Beta * [1 + (1 – Tax Rate) * (Debt / Equity)]

- Levered Beta = 1.08 * [(1 + (1 – 24.5%) * ($102.52 billion / $1,084.42 billion)]

- Levered Beta = 1.16

Given the above information, the levered beta of Apple Inc. for the year 2018 has been calculated as 1.16x.

Source Link: Apple Inc. Balance Sheet

Levered Beta Formula – Example #3

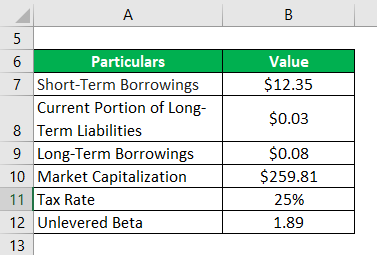

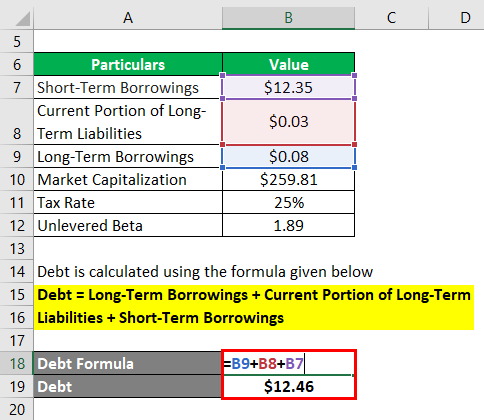

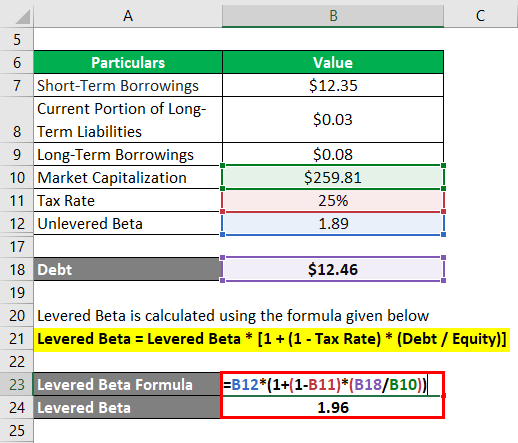

Let us now take the example of Samsung Electronics Co. Ltd. and use its annual report figures to calculate levered beta. According to available market information, the 1-year unlevered beta of the company stock is 1.89. During 2018, the company’s reported long-term borrowings, current portion of long-term liabilities and short-term borrowings stood at $0.08 billion, $0.03 billion and $12.35 billion respectively as on balance sheet. Calculate the levered beta of Samsung Electronics Co. Ltd if the current market capitalization is $259.81 billion, while the applicable corporate tax rate in South Korea is 25%.

Solution:

Debt is calculated using the formula given below

Debt = Long-Term Borrowings + Current Portion of Long-Term Liabilities + Short-Term Borrowings

- Debt = $0.08 billion + $0.03 billion + $12.35 billion

- Debt = $12.46 billion

Levered Beta is calculated using the formula given below

Levered Beta = Levered Beta * [1 + (1 – Tax Rate) * (Debt / Equity)]

- Levered Beta = 1.89 * [(1 + (1 – 25%) * ($12.46 billion / $259.81 billion)]

- Levered Beta = 1.96

Therefore, a levered beta of Samsung Electronics Co. Ltd. for the year 2018 stood at 2.55x.

Source Link: Samsung Balance Sheet

Explanation

The formula for the levered beta can be computed by using the following steps:

Step 1: Firstly, figure out the unlevered beta or asset beta of the company. The unlevered beta of listed companies is available at many stock market databases.

Step 2: Next, determine the company’s debt value from its balance sheet.

Step 3: Next, determine the company’s equity value, which is captured from its market capitalization. It can also be computed as stock’s trading price times the number of stocks free-floated in the market.

Step 4: Next, calculate the company’s leverage by dividing its debt (step 2) by its equity (step 3).

Debt-to-Equity Ratio = Debt / Equity

Step 5: Next, determine the effective tax rate of the subject company, which can be taken from its income statement or the applicable corporate tax rate can be used.

Step 6: Finally, the formula for the levered beta can be derived by multiplying unlevered beta (step 1) with a factor of 1 plus the product of debt-to-equity (step 4) ratio and (1 – tax rate) (step 5) as shown below.

Levered Beta = Unlevered Beta * [1 + (1 – Tax Rate) * (Debt / Equity)]

Relevance and Use of Levered Beta Formula

The concept of levered beta is important because it is one of the major lagging indicators used to assess the extent of volatility witnessed in the stock price of the subject company vis-à-vis the stock market index.

Typically, a levered beta value of 1 means that the stock’s risk is at par with the market risk, while a beta value of <1 means that the stock is less risky than the market and a beta of >1 means the stock is more riskier than the market risk.

Levered Beta Formula Calculator

You can use the following Calculator:

| Unlevered Beta | |

| Tax Rate | |

| Debt | |

| Equity | |

| Levered Beta | |

| Levered Beta = | Unlevered Beta * [1 + (1 -Tax Rate) * (Debt / Equity)] | |

| 0 * [1 + (1 -0) * (0 / 0)] = | 0 |

Recommended Articles

This is a guide to Levered Beta Formula. Here we discuss how to calculate Levered Beta Formula along with practical examples. We also provide a Levered Beta calculator with a downloadable excel template. You may also look at the following articles to learn more –