Difference Between Secured vs Unsecured Credit Card

A secured credit card is provided to its buyers only on the availability of some financial backing in the form of collateral before owning one. As the name suggests, this collateral provides a layer of security only in case of default. Here we will discuss the difference between Secured vs Unsecured Credit Card.

An unsecured credit card is provided to its buyers without any collateral commitment and is made more easily available to people in general. The unsecured cards form a part of the subprime market. Borrowers of both Secured vs Unsecured Credit cards can use these in all the outlets and places where they are acceptable. The credit limits provide the spending limit for the cardholder and must be repaid to maintain a good credit score.

Head To Head Comparison Between Secured vs Unsecured Credit Card (Infographics)

Below are the top 8 differences between Secured vs Unsecured Credit Card:

Key Differences Between Secured vs Unsecured Credit Card

Both Secured vs Unsecured Credit Card are popular choices in the market.

Let us discuss some of the major Difference Between Secured vs Unsecured Credit Card:

- The depositor collateral fixed for the type of card offered defines the key elements of each credit card. This makes a secured credit card different from the standard cards available for purchase. The credit limit that a customer thrives for in the case of a Secured Credit Card has to keep a minimum of that deposit or other collateral at least equivalent to the same limit. Rather than using the collateral for the regular monthly payments of the credit bills, it should only be used as a last resort.

- Many customers want a secured credit card to improve their credit scores. Since the chances of default and failure in repayment are lower, the cardholder meets the credit card bill requirements. In the case of unsecured corporate cards, since you do not have to commit any collateral, the lender has already assessed your credit history and is confident about your repayment ability.

- Many customers want unsecured credit cards to extend their credit limits. Keeping a deposit as a backup does not allow them to increase their credit limits often. Also, they want to use the same amount of deposit as a term deposit, which can give them some returns and not lie idle. We can extend the credit limit when customers make regular positive payments while keeping the deposit intact in the case of secured credit cards.

- In the case of regular positive payments towards the secured credit card, there are chances that the bank offers to upgrade to two options – increasing the credit limit or converting the card to an unsecured credit card. Having an upgrade to the unsecured card would mean that the entire security deposit amount or the collateral in full would be returned to the cardholder.

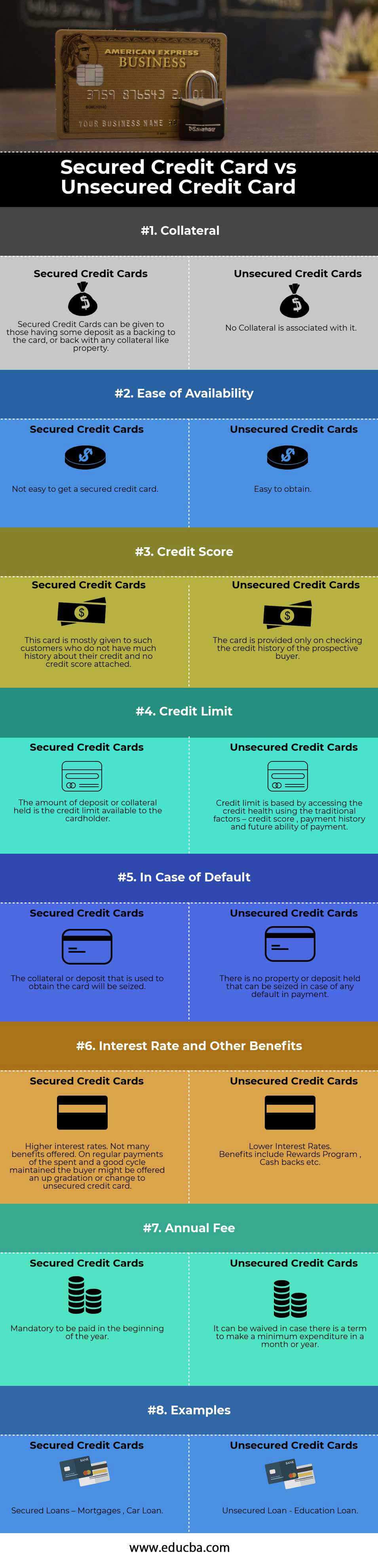

Secured vs Unsecured Credit Card Comparison Table

Below is the 8 topmost comparison between Secured vs Unsecured Credit Card

| Basis of Comparison | Secured Credit Cards | Unsecured Credit Cards |

| Collateral | We can give Secured Credit Cards to individuals who provide a deposit as a backing to the card or secure it with collateral like property. | No Collateral is associated with it. |

| Ease of availability | Not easy to get a secured credit card. | Easy to obtain. |

| Credit score | We mostly give this card to customers with limited credit history and no attached credit score. | The card is provided only by checking the credit history of the prospective buyer. |

| Credit limit | The amount of deposit or collateral held is the credit limit available to the cardholder. | A credit limit is based on accessing credit health using the traditional factors – credit score, payment history, and future payment ability. |

| In case of default | The collateral or deposit used to obtain the card will be seized. | There is no property or deposit held that can be seized in case of any default in payment. |

| Interest rate and other benefits | Higher interest rates. Not many benefits are offered. On regular payments of the spent and a good cycle maintained the buyer might be offered an up-gradation or change to an unsecured credit card. | Lower Interest Rates. Benefits include Rewards programs, Cash back, etc. |

| Annual fee | Mandatory to be paid at the beginning of the year | It can be waived if there is a term to make a minimum expenditure in a month or year. |

| Examples | Secured Loans – Mortgages, Car Loan | Unsecured Loan – Education Loan |

Conclusion

Credit cards are one of the best ways to keep a good credit score. One possible way is to keep the credit utilization ratio- the outstanding credit card balance ratio to the credit card limit. It measures the amount of credit limit being used. Secured credit cards require a security deposit; however, they are the safest compared to the unsecured credit option. It provides a way to improve your credit scores and your credibility in the market by making timely payments for the due amount. If you have an excellent credit score, you can opt or continue with unsecured credit cards. However, you will still qualify for the unsecured card if you have a fair credit score. Still, the interest rates over the period will become unfavorable, and the ease of owning depletes.

Recommended Articles

This has been a guide to the top difference between Secured vs Unsecured Credit Card. Here we also discuss the key differences between the Secured vs Unsecured Credit Card with infographics and a comparison table. You may also have a look at the following articles to learn more –