Updated July 24, 2023

Tax Shield Formula (Table of Contents)

What is the Tax Shield Formula?

Tax shields result from a necessary reduction in an individual’s or corporation’s taxable income by incorporating significant expenses into their total income, such as mortgage interest, medical expenditures, charitable donations, and depreciation.

The legitimacy and definition of deductions determine the variation of tax shields across countries. The value of the tax shield is contingent upon the effective tax rate applicable to the corporation or individual. Unclaimed tax losses from previous years can also lower the current year’s income compared to the previous year in certain cases.

Basically, the company uses two main tax shield strategies.

- Capital structure optimization.

- Accelerated depreciation methods.

1. Capital Structure: The impact of adding/ removing a tax shield is highly impacted by the company’s optimal capital structure, which is a mix of debt and equity funding. Moreover, the debt’s interest expense is tax deductible, making the debt funding cheaper.

2. Accelerated Depreciation: The depreciation expense is tax-deductible, where companies try to maximize the depreciation expenses to readily incorporate tax filings. Corporations use depreciation methods such as double declining balance and the sum of years – digits to lower taxes in the early years.

Tax shields are majorly used to further increase the cash flows and value of the business. Where the formula can determine the effect of the tax shield as such:

Examples of Tax Shield Formula (With Excel Template)

Let’s take an example to understand the calculation of Tax Shield in a better manner.

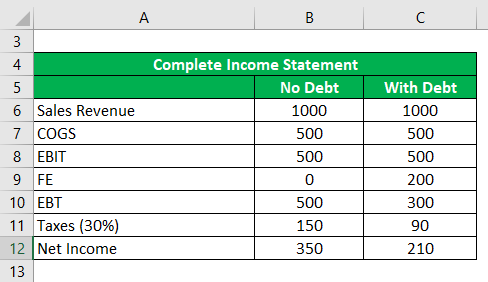

Tax Shield Formula – Example #1

Assume a firm with a Sales revenue of 1,000, a Cost of goods sold, COGS of 500, a Financial Expenses FE of 200, and a corporate tax rate of 30%. If we add financial expenses, what will be the final outcome?

Solution:

Here is a representation of the total outcome in tabular format, where taxes are calculated as follows:

TS = E (bt) * T

When the firm does not meet the Full TS as mentioned in the above calculation, then we firm follows either of the below-mentioned conditions:

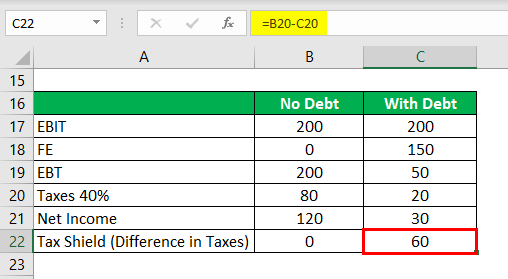

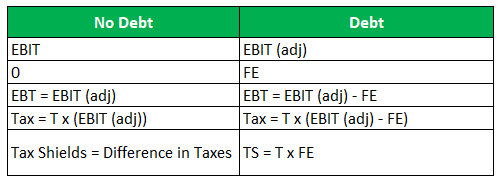

Table Shields when EBIT + OI > FE

When we increase FE from 0 to 150, in that case, net income decreases from 120 to 30, the net reduction is 90, and TS remains the same at 60. When EBT falls down to zero or negative, the firm doesn’t pay anything in that situation.

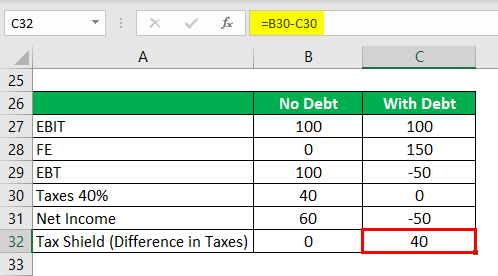

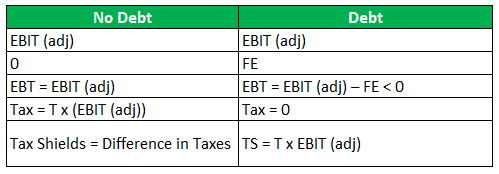

Table Shields when EBIT + OI < FE

Here, we have used the EBIT = 100, and FE has risen from 0 to 150, But net income drops to -50 from 60, which becomes 110, and TS remains at 40. In such a situation, it doesn’t pay taxes. Hence, Tax shields are not corporate tax rates times financial expenses.

In these criteria, Tax shields are corporate tax rate times EBIT plus other income when EBIT + IO < 0, Tax shields are zero.

Explanation

Tax Shield defines the additional expense on the bottom line as reduced. At certain conditions tax expense E(at) becomes E (bt) x (1-T). Hence

E(at) = E (bt) x (1-T)

TS = E (bt) x T

When the above-mentioned formula doesn’t meet the condition, Then EBIT(adj) plays a vital

Case 1: TS when EBIT(adj) >= FE when taxes are paid in the same period, and interest payments are the only source of TS.

Case 2: 0< EBIT(adj)< FE, when the firm doesn’t pay taxes and has no debt

Case 3: EBIT(adj) < 0, when EBIT(adj) is negative,the TS are zero

Where,

- EBIT = Earnings Before Interest and Tax

- EBIT(adj) = Earnings Before Interest and Tax Amount Offset Against Fe.

- FE = Financial Expences

- T = Corporate Tax

- TS = Tax Shield

Relevance and Use of Tax Shield Formula

Tax Shield minimizes the tax bills; it is the only reason taxpayers, individuals or corporations, spend a considerable amount of time determining how much tax levy or credit every year.

There are certain benefits of the tax shield strategy as such:

- Reduce the taxpayer’s taxable income for a given year or impose deferring income tax into future periods. In a similar way, we save the cash flows and increase the value of a firm.

- The strategy by which we minimize tax liability and increase the value of a business.

- It is the only way by which we can save cash outflows and appreciate the value of a firm. Tax shield in various other forms involves the type of expenditure deducted straight away from taxable income.

- A tax shield is the future tax saving attribute of tax by determining the firm’s present value. It helps predict a particular expenditure’s deductibility in the profit & loss account.

Recommended Articles

This is a guide to Tax Shield Formula. Here we discuss how to calculate Tax Shield along with practical examples. We also provide a downloadable Excel template. You may also look at the following articles to learn more –